Author: admin

WHITEPAPER: HOW TO SUCCESSFULLY SECURE REFINANCING IN THE TANK TERMINAL BUSINESS

Bunkerspot article

The Most Dramatic Year In The History Of Oil

There are very few industries in the world that have been hit as hard or are set to face as many consequences as the oil and gas industry in 2020. In a recent report, Fitch Ratings forecast that oil and gas exploration and production companies would lose $1.8 trillion in revenues this year, which is six times more than the retail sector is set to lose.

But the long-term consequences are going to be even more devastating. Perhaps the most visible change taking place in the oil and gas industry is the drastic cost-cutting measures being taken by the oil majors. BP has been forced to cut 10,000 jobs, or 15 percent of its workforce, as it tries to control costs in this new low oil price environment. Schlumberger had already slashed salaries and cut jobs in late March, while Shell and Chevron have announced plans to shrink their workforces.

And it isn’t just in the workforce where we are seeing unprecedented cuts. Shell’s decision to cut its dividend for the first time since 1945 was probably the single largest indicator of the long-term impact this pandemic will have on the oil industry. Shell and its fellow oil majors have prided themselves on paying out dividends regardless of market conditions in order to keep their shareholders happy. Its decision to cut its dividends marks a shift in strategy that suggests the oil major is now determined to cut its debt going forward and focus on financial sustainability rather than just pleasing shareholders.

It remains unclear if oil demand will ever return to pre-pandemic levels. From the destruction of the aviation industry to the transformation of workplace dynamics reducing daily travel and governmental pushes for renewable energy, oil demand is being attacked on all sides due to COVID-19. The oil majors seem to have recognized this global shift and are determined to make their operations as lean and sustainable as possible.

2020 is shaping up to be the most dramatic year in the history of oil markets, with a decade’s worth of change seeming to be taking place in just 365 days.

Author: Charles Kennedy, OilPrice.com – June 10, 2020

Trafigura posts record H1 oil trading earnings as market volatility soars

London — Trafigura, the world’s second-largest independent oil trader, said June 11 it benefited from “exceptionally strong” earnings from physical oil trading during the first half of the year when price volatility and supply dislocatoins spiked because of the coronavirus pandemic.

Register Now Reporting a 27% year-on-year jump in net profit for the first half to $542 million, Trafigura said its oil and petroleum products division delivered its highest H1 profit on record.

Gross profit from oil trading totaled $2.13 billion, up from $1.04 billion a year earlier and represented 68% of Trafigura’s total gross profit, the company said.

“At times like these, the physical trading and risk management activities of specialist companies such as Trafigura become more relevant than ever,” CFO Christophe Salmon said in a statement.

“The exceptionally strong performance in oil trading came in the context of significant volatility and dislocations in the global market for crude oil and refined products.”

Upbeat on H2

Trafigura said its shipping and chartering business also delivered a “very strong performance” having increased its fleet and equity position to benefit from anticipated IMO 2020 market disruption.

Brent crude prices dived over 60% over the first quarter to near two-decade lows after sweeping lockdowns hit demand and OPEC+ producers briefly abandoned their supply cut deal.

Demand for jet fuel was particularly hard hit, with 80% or more of the market disappearing as airlines grounded their fleets. Gasoline consumption also collapsed in many areas, Trafigura said.

“In the oil market, we saw, for a time, prices and curves moving from backwardation to contango and back again. Volatility broke all records,” Trafigura said.

Looking ahead, Trafigura said it expects to continue benefiting from market volatility in the H2 as the world economy slowly recovers from the pandemic.

“Trafigura is a highly resilient company that is providing reliable and valuable services to producers and consumers of vital commodities,” Salmon said. “…we see every reason to be confident that this will continue to be the case for the second half of our financial year.

Author: Robert Perkins, Editor: Felix Fernandez, Platts, June 11, 2020

Oil traders expect stocks to start falling this month

LONDON (Reuters) – Crude traders are anticipating a substantial reduction in global stocks over the next year as consumption recovers after the coronavirus epidemic and output cuts by OPEC+ and shale producers whittle away excess inventories.

Brent calendar spreads have tightened progressively since the middle of April as the major economies have begun to re-open after locking down in March and oil producers have started to cut output.

Brent futures’ six-month calendar spread has shrunk to a contango of less than $2 per barrel from a recent high of $12-$14 between late March and late April.

In the physical market, the five-week spread for dated Brent has flipped into a small backwardation of 15 cents per barrel from a contango of more than $6.

Brent spreads have historically been a good proxy for the global production-consumption balance as well as inventories in the United States.

Since the early 1990s, contango has corresponded with periods when the market was oversupplied and stocks have been rising year-on-year, while backwardation has correlated with falling stocks.

The recent shift from a wide contango towards a flat structure and even into backwardation for nearby dates therefore indicates stocks are expected to start falling soon, with the first draws in June or July.

Traders’ expectations expressed via the Brent spreads are consistent with the gradual drawdown in global oil stocks predicted by the major statistical agencies.

The U.S. Energy Information Administration forecasts U.S. crude inventories will fall by 230,000 barrels per day (bpd) in the second half of the year after increasing by more than 800,000 bpd in the first six months.

The agency predicts the U.S. market will move into a supply deficit of 200,000 bpd as early as July having been in surplus by 1.8 million bpd in April (“Short-Term Energy Outlook”, EIA, June 9).

U.S. commercial crude inventories (including stocks temporarily stored in the strategic petroleum reserve) are predicted to fall from 580 million barrels at end-June to 540 million by end-2020 and 510 million by end-2021.

OECD stocks of crude and products are forecast to decline almost 1.2 million bpd in the second half of 2020 and 0.8 million bpd in 2021, reversing an increase of 5.2 million bpd between March and May this year.

Globally, EIA forecasts inventories will fall by an average of 3.0 million bpd for the second half of 2020 after rising by at an average of 9.4 million bpd between January and May.

There is now a dominant view that the market will rebalance over the next 18 months, provided OPEC+ maintains its commitment to reduced production, U.S. shale output does not surge again, and there is no second wave of coronavirus.

(John Kemp is a Reuters market analyst. The views expressed are his own)

Author: John Kemp, Editor: Elaine Hardcastle, Reuters, June 10, 2020

New tests into degassing barges in North Sea Port successful

Testing of vapour processing installations began in Vlissingen, North Sea Port on Thursday 28 May. The aim is to enable inland tankers to process residual vapours safely and in a controlled manner with a newly developed installation. The initial tests were successful, North Sea Port says in a press release.

The industry has already achieved a significant reduction in emissions in recent years by introducing ’dedicated and compatible’ sailing, eliminating the need for degassing. However, this is not in itself sufficient to avoid degassing completely. In 2020, the prohibitions will therefore be gradually extended to a national ban that will reduce emissions of these harmful substances by 98%.

Degassing a vessel while sailing along inland waterways is bad for air quality, for the health of local residents and for people who work with these substances. Since 2015, the provinces of Zeeland, Noord-Brabant, Zuid-Holland, Utrecht, Noord-Holland, Gelderland and Flevoland have already introduced bans on the degassing of benzene and substances containing benzene.

The aim of the tests is to achieve cleaner air along the waterways with the help of innovative technologies. The tests at North Sea Port went well. The functioning of the equipment was monitored throughout the testing procedure.

These tests are the first of a series with different types of installations being rolled out in the ports of North Sea Port, Rotterdam and Amsterdam. The measurements are being conducted by an independent agency that will determine which installations meet the strictest requirements and where improvements are still needed. The results of the trials will be evaluated by the ‘degassing while sailing taskforce’, which will then advise the responsible Dutch minister on the further construction of the infrastructure.

The test in Zeeland is being supported by Shell Chemicals Europe. The site in Vlissingen has been provided by North Sea Port as part of its aim of achieving a more sustainable port. The province of Zeeland supports the project. Zeeland also currently holds the chairmanship of the national ‘degassing while sailing taskforce’. GreenPoint Maritime Services is supplying the vapour processing installation being used in the tests.

The Dutch Minister of Infrastructure and Water Management, Cora van Nieuwenhuizen, set up a ‘degassing while sailing taskforce’ in 2018 in order to ensure the smooth implementation of the national ban. From this year, the task force has been chaired by Dick van der Velde, a member of the Zeeland provincial executive. The task force includes representatives of central government, the provinces, ports, shippers, hauliers, storage companies and vapour processing firms. In order to facilitate the introduction of the national ban, it is important to build up an infrastructure consisting of innovative installations capable of processing or reusing the vapour cargo residues.

PortNews, June 9, 2020

Register for ARA Oil Tank Terminal Sample Report

Register today, to prepare for tomorrow!

Key learnings ARA Tank Terminal report

Important questions that need to be answered first before choosing a strategic direction. Recent events has shown just how volatile oil markets are and justifies in-depth market intelligence that enable intelligent decision making.

1. COVID-19: Covid-19 outbreak and its impact on oil markets.

2) IMO 2020 and changed bunkerfuel specs: Effect on fuel oil consumption, on MGO and growing storage demand.

3. Electrification of passenger cars: Downward effect on gasoline consumption and its positive impact on storage demand.

4. Reverse dieselization of European passenger car sales: Change in car sales might decrease structural imbalances and negatively impact storage demand.

Insights Global’s ARA Tank Terminal Annual Market Outlook Report will cover:

1) Our outlook for oil products supply, demand and trade flows and its impact on tanks storage demand.

2) Oil price forward curve outlook and its impact to tank storage markets

3) Tank storage capacity developments

4) Tank storage rates developments

5) View on medium term profitability

Themes that impact ARA Oil Tank Terminal Market

The tank terminal market in ARA is facing several challenges and issues that influence the short- and mid-term dynamics. Oil market developments, globally and regionally, could have an impact on the ARA Oil tank terminal market.

We have selected three main themes that impact ARA oil Tank Terminal markets in the short and medium term:

COVID-19 outbreak: Increase in tank demand and storage fees due to massive oversupply on petroleum markets (deep contango)

IMO 2020 and changed bunker fuel specifications: Growing ARA tank storage demand

Electrification of passenger cars: Downward effect on road fuels consumption but mixed effects on tank storage demand

Reverse dieselization of European passenger car sales: The change in car sales might decrease structural imbalances and lead to less demand for tank capacity

COVID-19 outbreak

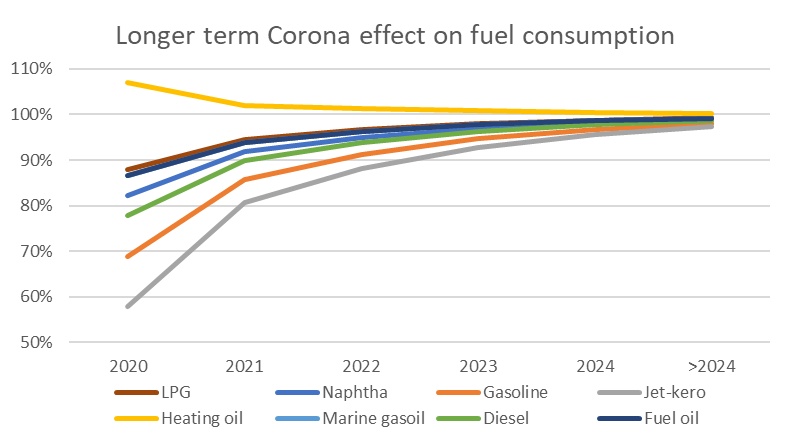

Since the beginning of the Corona crisis the market is clearly in contango. Looking to the calendar spread it was already expected that market would move into contango on a short term. However, the Corona crisis was the big trigger for the start of the contango period. As the graph shows the market is in a deep contango and how long this situation will persist is the main question. It depends on how fast the production and demand of oil products will become in balance again.

As we all experience the impact of Covid-19 is huge on our daily life and therefore also on our fuel consumption. The Corona effect needs to be incorporated on the forecasting models. Assumption is that the current lockdown lasts three months and has a negative impact for all fuels with the exception of heating oil. Reduction of diesel and LPG volumes are a bit lower because both diesel and LPG consumption is not limited to passengers’ vehicles. Commercial vehicles like buses and trucks don’t use gasoline fuels but usually diesel or LPG. Jet-kerosene is very much hit as almost all passenger traffic has stopped.

Reduction lockdown

LPG: 27%

Naphtha: 40%

Gasoline: 70%

Jet-kero: 95%

Heating oil: -20%

Marine gasoil: 30%

Diesel: 50%

Fuel oil: 30%

Reduction after lockdown in 2020

9%

13%

23%

32%

-3%

10%

17%

10%

After the lockdown, consumption level will gradually normalise, which will take five years. However, it is unclear yet what the exact impact of Covid-19 will be on the travel behaviour of people.

IMO 2020

The International Maritime Organization (IMO) has implemented its global legislation to limit sulphur emissions as a result of marine fuels. The legislation calls for a reduction of the sulphur content in marine fuels to less than 0.5%, which has started January 1st, 2020. Until the start of 2020 the limit was 3.5%. The first months of 2020 show that VLSFO seems to be the dominating bunker fuel. Consumption of MGO increased only slightly by around +10%. HFO is about 15-20% of total fuel oil consumption, with the rest being mostly VLSFO.

The consumption of bunker fuel is heavily correlated with global trade, so we expect it will take several years before bunker fuel market is at the same level as in 2019. However, terminals in ARA specialized in fuel oil will benefit from the growing size of the fuel oil bunker market. As the number of grades has increased and more components are needed to blend into the 0.5%FO / HSFO / MGO, more storage capacity is needed.

Additionally, on top of these structural effects on fuel oil supply, demand and imbalances, there is an enormous oversupply in the market due to the COVID-19 / Corona crisis. This has resulted in a steep contango in fuel oil forward prices and is stimulating traders to buy and store excess fuel oil supply. This provides major support for fuel oil storage rates in the short to medium term.

Electrification of passengers’ cars

Electric mobility is growing very fast. In 2018, the global electric car fleet exceeded 5.1 million, up 2 million from the previous year. China sold over 1 million cars in 2018, followed by Europe (385,000) and US (361,000). Norway has the highest market share for sales (46% in 2018). According to the IEA the projected growth in the New Policies Scenario of electric vehicles would cut oil products by 2.5 million barrels/day.

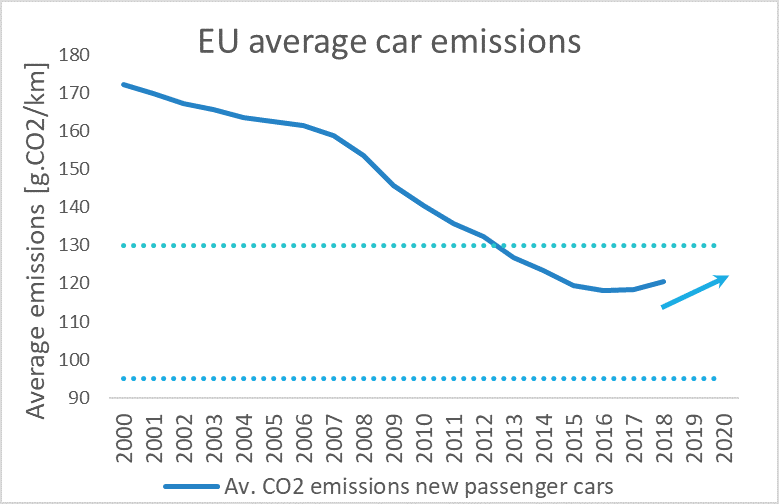

In a push to limit GHG emissions originating from vehicles the European Commission has imposed emission targets to car-producers. New cars are tested and need to have CO2 emissions lower than a certain limit. This limit has been gradually lowered to an average of 130 gram per kilometre in 2015 and will be lowered even further to 95 gram per kilometre as from 2021. CO2 emissions are directly proportional linked to fuel efficiency and therefore have a direct effect on consumption volumes per car per kilometre. As from 2025 the EU emission target is -15% relative to 2021. As from 2030 the target is set on -37.5% relative to 2021.

If car manufacturers do not comply to these targets, they will get penalties because of non-compliance. As BEV’s count as zero emissions cars, it is expected that these targets drive the production of electric cars.

However, reality is different as EU average car emissions are increasing again, see figure 5.6b. Higher SUV sales and not diesel decline have resulted in higher CO2 emissions.

Nevertheless, this electrification trend will have an impact on the gasoline consumption. In ARA the port of Amsterdam plays a central role in the gasoline segment. Because Europe has a structural surplus of gasoline there is a continuous flow being exported out of Europe to gasoline outlets. Consumption of European gasoline is expected to decrease, mainly because the electrification of its car fleet. As the production of gasoline will not decline or not decline that fast, it is expected that the surplus of gasoline will increase, which is beneficial for terminal operators.

Reverse dieselization of European passenger car sales

Due to a mix of governmental policies and changes in consumer preferences the share of diesel-powered cars relative to total cars sales has shifted dramatically in Northwest Europe. Consequently, the consumption of diesel is decreasing and it is expected this trend will continue. As production of diesel will not decline or not decline that fast, the deficit of gasoil / diesel is expected to decrease, which is not beneficial for terminal operators.

Conclusion

Although the oil market is really hit by Covid-19, the direct impact on oil terminal operators is positive as the market is currently in a deep contango. Consequently, tanks are rented out and storage fees have increased significantly.

Other themes like IMO 2020 and electrification of passenger cars seem to have positive effects on the profitability of terminal operators. IMO 2020 create more tank storage demand because of a higher number of bunker fuel grades and more components that are needed, while for gasoline the structural imbalance is expected to increase.

However, for the storage demand for diesel is expected to decrease because the current deficit is expected to decrease.

Having access to accurate, up-to-date oil storage rates is crucial to make the right business decisions.

With our Global Oil Storage Rate Report, you’ll gain access to the single and only authoritative source of storage rate information available worldwide. It will provide you with transparency on price levels in global tank storage markets regularly, so you are always in the know and can set the right ask and bid prices for your storage.

Download your FREE Sample Report now and discover what information you could have at your fingertips each quarter.

Costly Electric Vehicles Confront a Harsh Coronavirus Reality

For automakers who have invested heavily in a shift to high tech, there’s no turning back.

By Christoph Rauwald and Bruce Einhorn, 27 May 2020 (Bloomberg)

At a factory near Germany’s border with the Czech Republic, Volkswagen AG’s ambitious strategy to become the global leader in electric vehicles is coming up against the reality of manufacturing during a pandemic.

The Zwickau assembly lines, which produce the soon-to-be released ID.3 electric hatchback, are the centerpiece of a plan by the world’s biggest automaker to spend 33 billion euros ($36 billion) by 2024 developing and building EVs. At the site, where an East German automaker built the diminutive Trabant during the Cold War, VW eventually wants to churn out as many as 330,000 cars annually. That would make Zwickau one of Europe’s largest electric-car factories—and help the company overtake Tesla Inc. in selling next-generation vehicles.

But Covid-19 is putting VW’s and other automakers’ electric ambitions at risk. The economic crisis triggered by the pandemic has pushed the auto industry, among others, to near-collapse, emptying showrooms and shutting factories. As job losses mount, big-ticket purchases are firmly out of reach—in the U.S., where Tesla is cutting prices, more than 36 million people have filed for unemployment since mid-March. Also, the plunge in oil prices is making gasoline-powered vehicles more attractive, and some cash-strapped governments are less able to offer subsidies to promote new technologies.

Even before the crisis, automakers had to contend with an extended downturn in China, the world’s biggest auto market, where about half of all passenger EVs are sold. Total auto sales in China declined the past two years amid a slowing economy, escalating trade tensions, and stricter emission regulations. EV sales are forecast to fall to 932,000 this year, down 14% from 2019, according to BloombergNEF. The drop-off is expected to stretch into a third year as China’s leaders have abandoned their traditional practice of setting an annual target for economic growth, citing uncertainties. Economists surveyed by Bloomberg expect just 1.8% GDP growth this year.

Global Passenger Vehicle Sales

The global market contraction raises the prospect of casualties. French finance minister Bruno Le Maire has warned that Renault SA, an early adopter of electric cars with models like the Zoe, could “disappear” without state aid. Even Toyota Motor Corp., a hybrid pioneer when it first introduced the Prius hatchback in 1997, is under pressure. The Japanese manufacturer expects profits to tumble to the lowest level in almost a decade.

Automakers who for years have invested heavily in a shift to a high-tech future—including autonomous vehicles and other alternative energy-based forms of transportation such as hydrogen—now face a grim test. Do their pre-pandemic plans to build and sell electric cars at a profit have any chance of succeeding in a vastly changed economic climate? Even as Covid-19 has obliterated demand, for the car makers most committed to electric, there’s no turning back.

“We all have a historic task to accomplish,” Thomas Ulbrich, who runs Volkswagen’s EV business, said when assembly lines restarted on April 23, “to protect the health of our employees—and at the same time get business back on track responsibly.”

Volkswagen Pushes Ahead

Global EV sales will shrink this year, falling 18% to about 1.7 million units, according to BloombergNEF, although they’re likely to return to growth over the next four years, topping 6.9 million by 2024.

“The general trend toward electric vehicles is set to continue, but the economic conditions of the next two to three years will be tough,” said Marcus Berret, managing director at consultancy Roland Berger.

Volkswagen’s Zwickau facility became the first auto plant in Germany to resume production after a nationwide lockdown started in March. Before restarting, the company crafted a detailed list of about 100 safety measures for employees, requiring them to, among other things, wear masks and protective gear if they can’t adhere to social-distancing rules.

The cautious approach has reduced capacity—50 cars per day initially rolled off the Zwickau assembly line, roughly a third of what the plant manufactured before the coronavirus crisis. (VW said Wednesday that daily output had risen to 150 vehicles, with a plan to reach 225 next month.) Persistent software problems also have plagued development of the ID.3, one of 70 new electric models VW group is looking to bring to market in the coming years.

Still, Ulbrich and VW CEO Herbert Diess over the past three months have reaffirmed Volkswagen’s commitment to electrification. “My new working week starts together with Thomas Ulbrich at the wheel of a Volkswagen ID.3 – our most important project to meet the European CO2-targets in 2020 and 2021,” Diess wrote in a post on LinkedIn in April. “We are fighting hard to keep our timeline for the launches to come.”

Diess has described the ID.3 as “an electric car for the people that will move electric mobility from niche to mainstream.” Pre-Covid, the company had anticipated that 2020 would be the year it would prove its massive investments and years of planning for electric and hybrid models would start to pay off.

A more pressing worry that could hamper VW’s ability to scale up production is its existing inventory of unsold vehicles. The cars need to move to make room for new releases, but sales are down as consumers are tightening their spending. One response has been to offer improved financing in Germany, including optional rate protection should buyers lose their jobs. VW also has adopted new sales strategies first used by its Chinese operations, such as delivering disinfected cars to customer homes for test drives, and expanding online commerce.

Other German automakers are similarly pushing ahead with EV plans. Daimler AG is sticking to a plan to flank an electric SUV with a battery-powered van and a compact later this year. BMW AG plans to introduce the SUV-size iNEXT in 2021 as well as the i4, a sedan seeking to challenge Tesla’s best-selling Model 3.

A potential obstacle for all these companies—apart from still patchy charging infrastructure in many markets—is the availability of batteries. Supply bottlenecks appear inevitable given that the number of electric car projects across the industry outstrip global battery production capacity. And boosting cell manufacturing is a complicated task.

China’s (Weakened) EV Dominance

For VW and others, the first big test of EVs’ appeal in a Covid-19 world will come in China. Diess has referred to China as “the engine of success for Volkswagen AG.” VW group deliveries returned to growth year-on-year last month in China, while all other major markets declined.

Not long ago, China appeared to be leading the world toward an electric future. As part of President Xi Jinping’s goal to make the country an industrial superpower by 2025, the government implemented policies that would boost sales of EVs and help domestic automakers become globally competitive, not just in electric passenger cars but buses, too.

With the outbreak seemingly under control in much of the country, China is seeing some buyers return to the showrooms, but demand for passenger cars is likely to fall for the third year in a row, putting startups like NIO Inc. at risk and hurting more-established players like Warren Buffett-backed BYD Co., which suffered from a 40% year-on-year vehicle sales decline in the first four months of 2020.

The Chinese auto market may shrink as much as 25% this year, according to the China Association of Automobile Manufacturers, which before the pandemic had been expecting a 2% decline. EV sales fell by more than one-third in the second half of 2019.

NIO, the Shanghai-based startup that raised about $1 billion from a New York Stock Exchange initial public offering in 2018 but lost more than 11 billion yuan ($1.5 billion) last year, was thrown a much-needed lifeline when a group of investors, including a local government in China’s Anhui Province, offered 7 billion yuan last month.

Other Chinese manufacturers are counting on support from the government, too, including tax breaks and an extension to 2022 of subsidies, originally scheduled to end this year, to make EVs more affordable.

For now, the government will also look to help makers of internal combustion engine vehicles, at least during the worst of the crisis, said Jing Yang, director of corporate research in Shanghai with Fitch Ratings. But, she said, “over the medium-to-long term, the focus will still be on the EV side.”

America is Tesla Country

Companies can’t count on that same level of support from President Donald Trump in the U.S., where consumers who love their SUVs and pickup trucks have largely steered clear of electric vehicles other than Tesla’s.

The U.S. lags China and Europe in promoting the production and sale of EVs, and that gap may widen now that Americans can buy gas for less than $2 a gallon.

“When you’re digging out of this crisis, you’re not going to try to do that with unprofitable and low-volume products, which are EVs,” said Kevin Tynan, a senior analyst with Bloomberg Intelligence.

Weeks after announcing plans to launch EVs for each of its brands, General Motors Co. delayed the unveiling of the Cadillac Lyriq EV originally planned for April. Then on April 29, the company said it would put off the scheduled May introduction of a new Hummer EV. The models are part of CEO Mary Barra’s strategy to spend $20 billion on electrification and autonomous driving by 2025, to try to close the gap with Tesla.

In another move aimed at winning over Tesla buyers, Ford Motor Co. unveiled its electric Mustang Mach-E last November at a splashy event ahead of the Los Angeles Auto Show. The highly anticipated model had been scheduled to debut this year. Ford has not officially postponed the release, but the company has said all launches will be delayed by about two months, potentially pushing the Mach-E into 2021.

Elon Musk, whose cars dominate the U.S. electric market, cut prices by thousands of dollars overnight. The Model 3 is now $2,000 cheaper, starting at $37,990. The Model S and Model X each dropped $5,000.

Musk engaged in a high-profile fight with California officials this month over Tesla’s factory in Fremont, California, which had been closed by shutdown orders Musk slammed as “fascist.” In a May 11 tweet, he said the company was reopening the plant in defiance of county policy. On May 16, Tesla told employees it had received official approval.

During most of the shutdown in California, the company managed to keep producing some cars thanks to better relations with local officials regulating its other factory, in Shanghai. That plant closed as the virus spread from Wuhan in late January, but the local government helped it reopen a few weeks later in early February.

First Zwickau, Then the World

The ID.3’s new electric underpinning, dubbed MEB, is key to VW’s strategy to sell battery-powered cars on a global scale at prices that will be competitive with similar combustion-engine vehicles. Automakers typically rely on such platforms to achieve economies of scale and, ultimately, profits. MEB will be applied to purely electric vehicles across all of the company’s mass-market brands, including Skoda and Seat.

VW said it spent $7 billion developing MEB after Ford last year agreed to use the technology for one of its European models. Separately, the group’s Audi and Porsche brands are built on a dedicated EV platform for luxury cars that the company says will be vital in narrowing the gap with Tesla.

VW plans to escalate its electric-car push by adding two factories, near Shanghai and Shenzhen, that it says could eventually roll out 600,000 cars annually, more cars than Tesla delivered globally last year.

While China is the initial goal, making a dent in Europe and the U.S. is the long-term one. Like China, Europe had been tightening emissions regulations significantly before the pandemic. New rules to reduce fleet emissions will gradually start to take effect this year, effectively forcing most manufacturers to sell plug-in hybrids and purely electric cars to avoid steep fines.

Because of the mandates, Europe’s commitment to electrification isn’t going away, said Aakash Arora, a managing director with Boston Consulting Group. “In the long term, we don’t see any relaxation in regulation,” he said.

For VW, this crisis wouldn’t be the first time it started a new chapter in difficult times. Diess saw an opportunity coming off the manufacturer’s years-long diesel emissions scandal that cost the company more than $33 billion to win approval for the industry’s most aggressive push into EVs. When VW unveiled the ID.3, officials compared its historic role to the iconic Beetle and the Golf, not knowing that this might hold in unintended ways: The Beetle arose from the ashes of World War II, and the Golf was greeted by the oil-price shock in the 1970s.

“We have a clear commitment to become CO2 neutral by 2050,” VW strategy chief Michael Jost said, “and there is no alternative to our electric-car strategy to achieve this.”

- With assistance by Keith Naughton

- Photo by Eduardo Arcos on Unsplash