London, 11 October (Argus) — Oil product stocks held in independent storage within the Amsterdam-Rotterdam-Antwerp (ARA) trading hub fell by 2.4pc from a week earlier, largely as a result of a significant drop in fuel oil volumes. Stock levels of other products were broadly stable.

Fuel oil stocks fell by 17.3pc to 1.03mn t, prompted by the loading and departure of several cargoes during the week to today. The Max Jacob, booked by Litasco to ship 130,000t of HSFO to Singapore loaded on 4 October and headed eastbound. The South Sea, booked by P66 to ship 130,000t of cracked fuel oil from Rotterdam to Singapore, likely started loading on 11 October. Tankers also left the ARA area for west Africa and the Mideast Gulf. Arbitrage economics to take high-sulphur material from northwest Europe to Asia Pacific strengthened in the past week. The Singapore second-month 380cst swap premium to HSFO cargo prices in northwest Europe averaged $33/t on 4-10 October, compared with an average spread of $29.70/t during the prior five trading days. A total of 430,000t of fuel oil was booked to Singapore this week.

Gasoline stocks fell by 25,000t to 1.06mn t, with outflows being supported by efforts to sell off stored summer-grade volumes. Cargoes arrived in the ARA area from Finland, Spain and the UK. Tankers left the area for the Mideast Gulf, Brazil, Latin America and the Mediterranean. Naphtha stocks fell by 11,000t to 341,000t, prompted by steady demand from inland petrochemical end-users and low volumes arriving in the area. Tankers arrived from Algeria, France and Portugal, and none were seen departing.

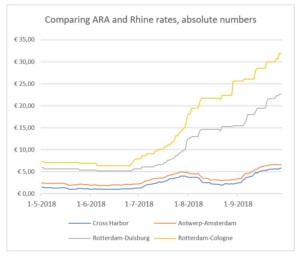

Stocks of gasoil rose by 102,000t to 3.04mn t, the highest level since mid-February 2018. Tankers arrived in the ARA area from Russia and Saudi Arabia, and departed for France, the Mediterranean and the UK. Low water levels on the river Rhine continued to impact barge traffic into Germany and France, bolstering interest in other forms of product transport. Cargo freight rates from the ARA continued to rise as a result, with some operators preferring to move material inland via other coastal outlets.

A single jet kerosene cargo arrived in the ARA area during the week to 11 October and a single tanker left for the UK. Inventories were effectively unchanged on the week at 674,000t. The Raysut partially offloaded in Rotterdam following a partial deposit into Fawley. The vessel had been sitting in the English Channel since 18 June, as the buyer was exercising some of its contract options by waiting to offload. Northwest European jet fuel demand has fallen since last week. Imports from east of Suez have been thin, with most arrivals entering UK and French ports.

Reporter: Thomas Warner