Insights from Lars – comparing ARA and Rhine freight rates over the summer.

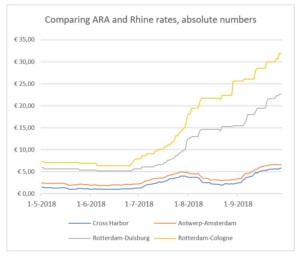

Freight rates in both the ARA region as well as on the Rhine remained strong, supported by increasing demand and the ongoing low water levels, which are hampering intakes. Freight rates for Rhine based destinations have not only risen for Middle and Upper Rhine destinations, where loaded volumes are contracted by low water levels up pegel Kaub, but also destinations in the German Ruhr area are highely affected. The difference between ARA-routes like Cross Harbor transports, Antwerp – Amsterdam and Rhine based tranports to Duisburg or Cologne are shown below.

In common situations, freight rates per mton are increasing in line with the voyage durations. The strong demand, and therefore increasing rates, to German markets are seen in the two graphs. Besides the absolute freight rates, a graph is made for indexed freight rates. The base rates of 1st of May 2018 are used for this calculation. After a slow late-spring, with low freight rates per ton, rates started to increase from July on. This has been accelerated by decreasing water levels and increasing demand for automotive fuels in hinterland markets. Rates to the Ruhr area, which are longer voyages compared to ARA-transports and are therefore priced at higher levels, saw a steady increase during the summer season. In August, a distinction is seen between demand in ARA, which was fading, and up the Rhine, which was supported by diesel transports.

Last month, rates up the Rhine increased further. Water levels continued to stay low and the market regained support from outages at various refineries in Germany. The maintenance season is causing less local supply and an unplanned outage at the Vohburg refinery in Bavaria is limiting product supply even further. Importers are looking at alternative outlets and more product needs to be imported to handle domestic demand. This is partly done over the Rhine, where barges are still coping with loading restrictions. Imports by barge have however increased by over 60% during September compared to the summer months, as was seen in PJK’s Rhine barge flow reports. By comparison, rates to Lower Rhine destinations have more than quadrupled in the last months. The revenue per barge is somewhat lower due to less loaded volumes, but are still elevated. This is also seen in the ARA, where supply of barges is lacking due to the higher demand in Germany. The demand for importing product in the coming weeks could remain high since end consumers still need to stock up heating oils for the winter. This has been postponed last spring due to the backwardated market structure, so stock levels in hinterland are relatively low. With inadequate local production, low availability of barges and high freight rates, keeping track of the markets is vital in order to stay up to date.

If you would like more information about our products like the Rhine flow service, barge freight rates and daily reports, contact our sales department in the Netherlands at +31 850 66 25 00 or at info@insights-global.com.