Oil and gas companies, as well as the retail industry, are the worst hit sectors in the COVID-19 pandemic that swept through businesses in Texas, bankruptcy and restructuring lawyers say.

According to data provided exclusively to The Texas Lawbook by Androvett Legal Media research, more than 545 companies of all sectors in Texas filed for Chapter 11 protection from creditors between January 1 and May 5, 2020. This is a surge of 133 percent compared to the same period of 2019, Mark Curriden at The Texas Lawbook writes in Houston Chronicle.

Within Texas, Houston is the center of the wave of bankruptcies, which include many names in the retail and oil industries, according to the data and to bankruptcy partners at law firms.

In April, companies such as Diamond Offshore Drilling and Whiting Petroleum filed for Chapter 11 bankruptcy protection. U.S. shale gas pioneer Chesapeake Energy said in May it was evaluating a Chapter 11 bankruptcy protection reorganization—along with other options—as the low oil and gas prices weigh heavily on its finances and substantial outstanding debt.

The list is set to grow in coming weeks, according to legal experts.

“Oil and gas and the retail sector had a whole lot of stress even before COVID-19. The only surprising thing is that we haven’t seen the explosion of bankruptcy filings already. But they are still coming,” Lou Strubeck, head of the bankruptcy and restructuring practice at Norton Rose Fulbright, told The Texas Lawbook’s Mark Curriden.

According to Strubeck, creditors are not rushing for court reorganizations of energy companies because “they don’t know what they would do with the assets and they don’t want to run these companies.”

With less capital to invest in bankruptcy restructuring of oil firms than in the 2015-2016 downturn, private equity could sit on the sidelines, and we may see more “free fall” bankruptcies and fewer prepackaged bankruptcies, Matthew Cavanaugh, a bankruptcy partner with Jackson Walker in Houston, told The Texas Lawbook.

Investors were shocked on April 20 when oil futures set for May delivery fell below zero for the first time ever . Although the negative oil prices lasted less than 24 hours, the plunge started a debate about whether it could happen again this month with the June futures.

In the days after the price first plunged, some analysts predicted it could happen again , because the dynamics in the market weren’t expected to change. But that now looks increasingly unlikely—both because of the dynamics of crude trading and because the oil market isn’t in as dire straits as it was two weeks ago. West Texas Intermediate crude futures have rallied more than 40% this month, to above $23 a barrel.

“No June will not go negative,” Richard Redoglia, CEO of Matrix Global, wrote in an email. “It might see some weakness, but the panic is over.” Matrix Global runs auctions for crude storage space.

To see why, it helps to understand oil trading.

West Texas futures—the financial instrument that went negative—give investors a unique way to track the oil market. They are contracts that result in the buyer receiving barrels of crude oil after the contracts expire. By comparison, Brent crude, the international oil benchmark, settles in cash. People who own West Texas crude on the day the contracts expire have to be prepared to receive 1,000 barrels of oil. Usually, that isn’t a problem because buyers can rent storage tanks in Cushing, Okla., the delivery point. But in April, all of the storage in Cushing was booked, so traders who were still holding the contract near expiration couldn’t put it anywhere. And no one wanted to buy the contracts. So they fell to negative $40 a barrel, implying that sellers would pay buyers $40,000 per contract.

Some of those dynamics are still in place. Covid-19 shutdowns have led to reduced oil demand, so oil producers have nowhere to put the oil they are pumping out. Instead of refining it into gasoline, they are putting more of it into storage. So storage is still tight in Cushing. People holding June futures won’t find much storage available for purchase.

But other dynamics make a negative prices less likely. For one thing, traders know that negative prices are theoretically possible. Before April, it wasn’t clear to many traders that negative prices were possible; the Chicago Mercantile Exchange adjusted its computer systems to allow for normal trading at negative prices in April. “The element of surprise is gone,” CFRA Research analyst Stewart Glickman wrote in an email.

Going into the weekend before the expiration of the May contract, there were more than 100,000 open contracts still trading. Many of those people probably expected to be able to sell them or roll those contracts over to the June contract. But come Monday, no one wanted to touch the May contracts, because they were trading at a deep discount to the June contracts. The pattern is known as contango, where oil set for delivery in future months is worth more than it is today, because people expect more people to be using oil in the future (in this case, because Covid-19 shutdowns are expected to ease).

Oil is still in contango today, but it isn’t nearly as steep as it was then. At its height, the spread between the June and July contract was about $6. Today, that spread is less than $2. And the biggest crude buyers have mostly avoided buying into the June contract, instead shifting their bets to July. The U.S. Oil Fund exchange-traded fund (ticker: USO), the most popular way for investors to bet on the price of crude, has already rolled out of the contract and into later-dated months. Open interest in the June contract is at less than half the level it was for the May contract at the same point, according to a report from ING on Thursday.

That has made the June contract less precarious. If most traders move out of it early, there won’t be many stuck looking for storage on the date of expiration again.

The new dynamic suggests that “market participants who do not have the capability to take physical delivery will likely not hold their position in the final days of the contract’s life,” Warren Patterson, head of commodities strategy at ING, wrote in the report.

Beyond the trading dynamics, the oil market has been moving closer toward balance in recent days. Producers around the world have cumulatively reduced their output by more than 10%, and demand has slowly started to return as countries have begun reducing restrictions on movement. As oil held in storage starts getting used for gasoline and diesel, Cushing tanks may open up too.

Nonetheless, some analysts think the recent rally in oil prices could fade. Glickman doesn’t expect oil to go negative, but he also doesn’t expect things to be hunky-dory for a while.

“With all that said, I’m still not a believer in this oil rally,” he wrote. “Prices don’t have to go negative to worry about rising storage and terrible visibility about the extent to any demand recovery.”

Do you want to stay up-to date with the key insights and developments you need to determine your strategy as a Tank Terminal Operator? Are you planning to invest in a tank terminal, but do you need a more in-depth understanding of the oil market dynamics and its impact on tank terminals? Do you need an outlook to make better business decisions?

Important themes for tank terminal market in ARA are:

1) COVID-19 outbreak and its impact on the oil market 2) IMO 2020 and changed bunker fuel specifications: Effect on fuel oil consumption, on MGO and growing ARA tank storage demand 3) Electrification of passenger cars: Downward effect on gasoline consumption and its positive impact on ARA tank storage demand 4) Reverse dieselization of European passenger car sales: The change in car sales might decrease structural imbalances and has a negative impact on ARA tank storage demand

The ARA Tank Terminal Annual Report will cover:

1) Our outlook for oil products supply, demand and trade flows and its impact on tanks storage demand. 2) Oil price forward curve outlook and its impact to tank storage markets 3) Tank storage capacity developments 4) Tank storage rates developments 5) View on medium term profitability

Fill in your contact details below if you would like to purchase this report which contains a unique view on current tank storage market fundamentals.

Syed Shah usually buys and sells stocks and currencies through his Interactive Brokers account, but he couldn’t resist trying his hand at some oil trading on April 20, the day prices plunged below zero for the first time ever. The day trader, working from his house in a Toronto suburb, figured he couldn’t lose as he spent $2,400 snapping up crude at $3.30 a barrel, and then 50 cents. Then came what looked like the deal of a lifetime: buying 212 futures contracts on West Texas Intermediate for an astonishing penny each.

What he didn’t know was oil’s first trip into negative pricing had broken Interactive Brokers Group Inc. Its software couldn’t cope with that pesky minus sign, even though it was always technically possible — though this was an outlandish idea before the pandemic — for the crude market to go upside down. Crude was actually around negative $3.70 a barrel when Shah’s screen had it at 1 cent. Interactive Brokers never displayed a subzero price to him as oil kept diving to end the day at minus $37.63 a barrel.

At midnight, Shah got the devastating news: he owed Interactive Brokers $9 million. He’d started the day with $77,000 in his account.

“I was in shock,” the 30-year-old said in a phone interview. “I felt like everything was going to be taken from me, all my assets.”

To be clear, investors who were long those oil contracts had a brutal day, regardless of what brokerage they had their account in. What set Interactive Brokers apart, though, is that its customers were flying blind, unable to see that prices had turned negative, or in other cases locked into their investments and blocked from trading. Compounding the problem, and a big reason why Shah lost an unbelievable amount in a few hours, is that the negative numbers also blew up the model Interactive Brokers used to calculate the amount of margin — aka collateral — that customers needed to secure their accounts.

Thomas Peterffy, the chairman and founder of Interactive Brokers, says the journey into negative territory exposed bugs in the company’s software. “It’s a $113 million mistake on our part,” the 75-year-old billionaire said in an interview Wednesday. Since then, his firm revised its maximum loss estimate to $109.3 million. It’s been a moving target from the start; on April 21, Interactive Brokers figured it was down $88 million from the incident.

Customers will be made whole, Peterffy said. “We will rebate from our own funds to our customers who were locked in with a long position during the time the price was negative any losses they suffered below zero.”

That could help Shah. The day trader in Mississauga, Canada, bought his first five contracts for $3.30 each at 1:19 p.m. that historic Monday. Over the next 40 minutes or so he bought 21 more, the last for 50 cents. He tried to put an order in for a negative price, but the Interactive Brokers system rejected it, so he became more convinced that it wasn’t possible for oil to go below zero. At 2:11 p.m., he placed that dream-turned-nightmare trade at a penny.

It was only later that night that he saw on the news that oil had plunged to the never-before-seen price of negative $37.63 per barrel. What did that mean for the hundreds of contracts he’d bought? He frantically tried to contact support at the firm, but no one could help him. Then that late-night statement arrived with a loss so big it was expressed with an exponent.

The problem wasn’t confined to North America. Thousands of miles away, Interactive Brokers customer Manfred Koller ran into trouble similar to what Shah faced. Koller, who lives near Frankfurt and trades from his home computer on behalf of two friends, also didn’t realize oil prices could go negative.

He’d bought contracts for his friends on Interactive Brokers that day at $11 and between $4 and $5. Just after 2 p.m. New York time, his trading screen froze. “The price feed went black, there were no bids or offers anymore,” he said in an interview. Yet as far as he knew at this point, according to his Interactive Brokers account, he didn’t have anything to worry about as trading closed for the day.

Following the carnage, Interactive Brokers sent him notice that he owed $110,000. His friends were completely wiped out. “This is definitely not what you want to do, lose all your money in 20 minutes,” Koller said.

Besides locking up because of negative prices, a second issue concerned the amount of money Interactive Brokers required its customers to have on hand in order to trade. Known as margin, it’s a vital risk measure to ensure traders don’t lose more than they can afford. For the 212 oil contracts Shah bought for 1 cent each, the broker only required his account to have $30 of margin per contract. It was as if Interactive Brokers thought the potential loss of buying at one cent was one cent, rather than the almost unlimited downside that negative prices imply, he said.

“It seems like they didn’t know it could happen,” Shah said.

But it was known industrywide that CME Group Inc.’s benchmark oil contracts could go negative. Five days before the mayhem, the owner of the New York Mercantile Exchange, where the trading took place, sent a notice to all its clearing-member firms advising them that they could test their systems using negative prices. “Effective immediately, firms wishing to test such negative futures and/or strike prices in their systems may utilize CME’s ‘New Release’ testing environments” for crude oil, the exchange said.

Interactive Brokers got that notice, Peterffy said. But he says the firm needed more time to upgrade its trading platform.

“Five days, including the weekend, with the coronavirus going on and a complex system where we have to make many changes, was not a sufficient amount of time,” he said. “The idea we could have bugs is not, in my mind, a surprise.” He also acknowledged the error in the margin model Interactive Brokers used that day.

According to Peterffy, its customers were long 563 oil contracts on Nymex, as well as 2,448 related contracts listed at another company, Intercontinental Exchange Inc. Interactive Brokers foresees refunding $18,815 for the Nymex ones and $37,630 for ICE’s, according to a spokesman.

To give a sense of how far off the Interactive Brokers margin model was that day, similar trades to what Shah placed would have required $6,930 per trade in margin if he placed them at Intercontinental Exchange. That’s 231 times the $30 Interactive Brokers charged.

“I realized after the fact the margin for those contracts is very high and these trades should never have been processed,” he said. He didn’t sleep for three nights after getting the $9 million margin call, he said.

Peterffy accepted blame, but said there was little market liquidity after prices went negative, which could’ve prevented customers from exiting their trades anyway. He also laid responsibility on the exchanges and said the company had been in touch with the industry’s regulator, the U.S. Commodity Futures Trading Commission.

“We have called the CFTC and complained bitterly,” Peterffy said. “It appears the exchanges are going scot-free.”

Representatives of CME and Intercontinental Exchange declined to comment. A CFTC spokesman didn’t immediately return a request for comment.

The fallout for retail investors like Shah and Koller raises questions over whether they should’ve been allowed to take a position in oil contracts right before they expired, putting them in position to have to take possession of barrels of crude oil. Brokers have been grappling with how to shield clients, especially those with small accounts who are clearly incapable of taking physical delivery, since that day. Some, including INTL FCStone, have already blocked certain clients from touching the front-month oil futures contract.

Peterffy said there’s a problem with how exchanges design their contracts because the trading dries up as they near expiration. The May oil futures contract — the one that went negative — expired the day after the historic plunge, so most of the market had moved to trading the June contract, which expires May 19 and currently trades above $24 a barrel.

“That’s how it’s possible for these contracts to go absolutely crazy and close at a price that has no economic justification,” Peterffy said. “The issue is whose responsibility is this?”

Just a few years ago the head of ExxonMobil had to appear before a Congressional committee to explain their billions of dollars in profits that some called “obscene.”

This week investors in ExxonMobil are asking why the company did not make any profit during the first quarter of 2020. Its $610 million loss is the first time that ExxonMobil reported a loss in more than 30 years.

ExxonMobil isn’t the only oil company reporting financial troubles. Actually, there are more losers than winners.

The United States Oil Fund, the largest crude exchange traded product, said recently it will sell all of its 30-day contracts to avoid a repeat of the heavy losses that occurred around the expiration of the May contract on April 20 when the price of oil bottomed out at -$37 per barrel.

Crude oil inventories continue to rise indicating the oversupply is still expanding. The Energy Information Administration reported on Wednesday inventories increased by 4.6 million barrels from 527 million barrels to 532 million barrels. It is the 14th consecutive week that inventories increased.

Oil prices on the New York Mercantile Exchange for June delivery increased early in the week to $25 but declined to $23 after inventory figures were announced. Posted price for lease sales in Texas varied from $21 in North and West Central to $14 in South Texas, according to the Texas Alliance of Energy Producers web page.

The S&P Dow Jones Indices announced last week it would “pre-roll” all June West Texas Intermediate contracts to July for all of its commodity indices given the risk of June falling to or below zero given limited storage capacity.

Even though many U.S. oil producers intend to cut their production, it takes time to work out the details. Which wells will be cut back? Can they be shut down entirely? What’s the cost? Will there be damage to the well? What problems could be encountered restarting production? What about contracts with partners, royalty owners, drilling contractors and other service providers?

The EIA reports that U.S. production has dropped since a high of 13.1 million barrels per day in February to 12.8 this week. ExxonMobil, Chevron and ConocoPhillips all say they will reduce production that will total about 1.2 million b/d this year.

Many companies that purchase crude oil at the lease from smaller independent producers have told their customers they will not purchase any oil after May 15 because storage facilities are near capacity and there is no place to store the oil.

Refinery run fell to 12.8 million b/d for the week ending April 24, which is 21 percent lower than the five-year average. Demand for gasoline and jet fuel dropped to a 30-year low and an oversupply exists. Retail gasoline prices across the U.S. averaged $1.789 per gallon last week, which is a decline of $1.108 from the same period in 2019 …

The U.S. rig count declined by 57 last week to 408. The rig count last year on May 1 was 990. The huge decline indicates that producers will have difficulty replacing reserves and production when prices rebound.

There is a light at the end of the tunnel, however. Economists expect demand for petroleum products will strengthen as economic activity increases following the easing to restrictions on travel and business activity.

Will ExxonMobil be able to survive? Time will tell. As the global economy rebounds so will the demand for petroleum products and the bottom line for oil producers in Texas and around the world.

LONDON — Global fuel oil

demand may be holding up better than its jet fuel and gasoline peers, but with

inland storage facilities at high levels it appears only a matter of time

before the economics of floating storage in Europe start to make sense for the

marine fuel, according to market sources.

Shipping’s importance to the

world economy — 90% of global trade is seaborne — means it has been given

exemptions to keep operating through the widespread global lockdowns. However,

the coronavirus pandemic has not left fuel oil demand unscathed as dry bulk,

cruise ships and the container market all suffer, with inland builds of stocks

in Europe and stocks spilling over on to floating storage in Singapore.

Combined stocks of fuel oil in the

Amsterdam-Rotterdam-Antwerp hub decreased nearly 12% to 1.357 million mt in the

seven days to Wednesday, according to data from Insights Global, but this was

after reaching a 21-month high the previous week.

“Storage is pretty full, and demand is

dire,” a source said, adding that buyers are pushing back delivery dates

for product. The source noted however that 0.5% sulfur fuel oil demand is “a

little healthier” compared to other fuel oil grades “as bunker

volumes seem OK.”

“The fuel oil contango is not enough to

incentivize floating storage; it works better for inland storage,” another

source said. Other sources noted that the contango on 0.5% marine fuel works

better than for high sulfur fuel oil, so it is being prioritized in the queue

for storage.

Indeed, there appears to a global pecking order

for storage related to the decimation of demand and the premium that can be

commanded when they do sell, with crude, jet and gasoline all being moored

offshore in considerable volumes. S&P Global Platts Analytics notes that

all forward curves are all deeply in contango which is consistent with stock

builds with jet, gasoline, and diesel, but the HSFO trend is similar albeit

lagging.

Not all fuel oil is equal

Demand for 3.5% fuel oil after the

International Maritime Organization’s stricter sulfur cap that came in to force

January 1, 2020 has fallen off for the bunker pool as scrubber economics —

using an exhaust cleaning system to allow vessels to continue burning high sulfur

fuel — come in to question. One source noted however they were looking to

store all fuel oil grades.

In the paper market, the time spread between

3.5% FOB Rotterdam barge front-month and month two was last assessed Thursday

in a minus $12/mt contango, widening from minus $10.25/mt the day before.

The 0.5% FOB Rotterdam barges spread was

assessed at minus $14.50/mt, steepening from minus $13.00/mt Wednesday and from

minus $8.00/mt at the start of the month.

“0.5% marine fuel has a better contango, I

am not surprised that more people are positioning themselves to store

that,” one fuel oil source said.

Storage running out

As a result of limited storage capacity,

European bunker premiums — the delivered market compared to the respective

barge prices — have come under pressure recently, falling steadily since

February. So far in April the premium has averaged $8.94/mt, down from a March

average of $19.41/mt and off sharply from the February average of $26.24/mt.

One bunker source noted a decline in bunker

premiums last week, particularly for Mediterranean marine gasoil, adding that

this could be a result of needing to free up space for more product coming in.

The markets are keeping an eye on storage

fundamentals, and not ruling floating storage out as it remains the only option

after inland storage becomes saturated, which participants may be pushed to do

so despite being uneconomic in the near future.

“Availability and prices of vessels will

rally, so there will be less vessels and those that are left would be more

expensive,” a source said.

“Some are starting to look at floating

storage,” another source said, adding that they wouldn’t be surprised if

some started to store on vessels.

Platts Analytics sees inland storage running

out by June, with total storage afloat potentially increasing by 250 million

barrels.

Fuel oil won’t have long to jump aboard those

ships and the move to store fuel oil on the water in Europe may not be far

away.

As we are now in the second quarter of 2020 it is time to look back on the introduction of the IMO legislation on the regulation of sulphur emissions from bunker fuels. The dust has settled with respect to the implementation of these new rules. But as this happened a ‘black swan’ arrived on the global oil scene: COVID-19 or the Corona virus. This virus and the international crisis it evoked is gripping international trade and impacting shipping and bunker sales like nothing we’ve ever seen before. So, this article will also look forward to estimating the medium-term impact on bunker markets and in particular on bunker storage markets.

Running up to 2020

The International Maritime Organization (IMO) has implemented its global legislation to limit sulphur emissions as a result of marine fuels. The legislation calls for a reduction of the sulphur content in marine fuels to less than 0.5%, which has started January 1st, 2020. Until the start of 2020 the limit was 3.5%.

Leading up to the start of this new era in marine fuels there have been multiple opinions or scenarios about which bunker fuels would become dominant. In first instance, most stakeholders thought HSFO would remain the dominant bunker fuel because of the expected uptake of scrubbers. Other stakeholders assumed that MGO would become the dominant bunker fuel as there wouldn’t be enough supply of 0.5% FO. In 2018/2019 some oil majors, IEA and consultants changed their opinion believing that VLSFO would become the dominant fuel. There were other stakeholders, like the gasoil traders, who thought that the demand of MGO would increase significantly because of IMO 2020.

The first months of 2020

The first months of 2020 show that VLSFO seems to be the dominating bunker fuel. Consumption of MGO increased only slightly by around +10%. HFO is about 20% of total fuel oil consumption, with the rest being mostly VLSFO.

The introduction of the new 0.5%FO, called VLSFO, has led to some compatibility concerns. VLSFO blends can come from residual components and distillate components. Residual components are mostly aromatic due to the asphaltenes in the bottom of the barrel. Distillates are high on paraffins. Blending these two streams together can lead to compatibility issues. This can occur if a ship switches between different batches and the fuel is mixed in the ship’s fuel tank, a process also known as co-mingling. Co-mingling bunker fuels from different origins could lead to serious damage to engines or clogging of fuel lines. VLSFO residue blends, being more aromatic and hydrotreated vacuum gasoil (VGO), being less aromatic have these compatibility issues.

These compatibility issues also have a positive impact on the demand for storage capacity as some product owners avoid co-mingling new fuels in their tanks. So, this calls for segregated tanks, which will increase demand for tanks.

An important and lucrative business for oil traders in the ARA-region used to be the transhipment of fuel oil from Russia to the Far East. However, this transit flow has largely disappeared. On the one hand supply of Russian fuel oil has gone down whereas demand for fuel oil in Asia has dropped significantly. Furthermore, Asian bunker demand for fuel oil is currently be supplied from other sources more nearby. Nowadays, Russian export are directly exported in smaller tankers, with as main destination the US. ARA is not the place anymore where making bulk for HFO takes place.

Looking forward

Our assumption in the post 2020 era is that the shipping industry will keep on using FO as the dominant marine fuel (80%). Unclear is what the share of each VLSFO and HSFO will be.

In our forecasting models the Corona effect is incorporated. Assumption is that the current lockdown lasts three months and has a negative impact on marine fuel bunker consumption levels. After the lockdown, consumption level will gradually normalise, which will take five years. Our assumption of five years is based on experience in the past and the enormous fall of GDP which influences the consumption of fuel oil. IMF forecasts a contraction of the global GDP of 3% in 2020, while the Eurozone will see a decline of 7.5% in 2020. It will take several years of GDP growth to be back at the same GDP level as in 2019. The consumption of bunker fuel is heavily correlated with global trade, so we expect it will take several years before bunker fuel market is at the same level as in 2019.

Due to growing bunker fuel consumption and declining average production, surplus in NW Europe will change into a deficit. Terminals in ARA specialized in fuel oil will benefit from the growing size of the fuel oil bunker market. As the number of grades has increased and more components are needed to blend into the 0.5% FO / HSFO / MGO, more storage capacity is needed.

Additionally, on top of these structural effects on fuel oil supply, demand and imbalances, there is an enormous oversupply in the market due to the COVID-19 / Corona crisis. This has resulted in a steep contango in fuel oil forward prices and is stimulating traders to buy and store excess fuel oil supply. This provides major support for fuel oil storage rates in the short to medium term.

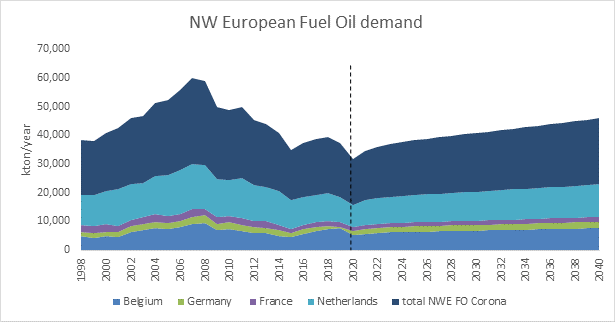

Figure 1: NWE HFO demand Forecast

So summarizing, the introduction of IMO 2020 fuel oil regulations and the COVID-19 / Corona crisis have had the following impact: 1) More tanks needed to segregate blend and fuel grades 2) Less arbitrage flows limit demand for large tanks 3) Long term bunker demand growth and rising imbalances will support tank demand 4) Short to medium term support of fuel oil storage rates due to steep contango

The real impact of Corona on the global and regional GDP’s is not clear yet, but we may conclude that the IMO 2020 regulation have had a positive impact on the ARA tank storage demand. Also in the short to medium term, the COVID-19 / Corona crisis have had a positive effect on the tank terminal business.

The COVID-19 virus has a huge impact on the global oil market. The virus and the economic crisis it evoked results in a large decline of the oil demand. I this article we will describe the consequences of this drop in consumption on the tanks storage demand in main oil hubs.

A collaboration between Q88 and Insights Global, updated version

In the world of the liquid storage some 5,000 terminals can be identified. These terminals have different kind of functions. A terminal’s main function is to balance supply with demand, they can act as import terminal, as trading platform or offer strategic storage options.

Q88 and Insights Global are proud to partner to bring our clients timely information. Never before has the relevance of these terminals been highlighted, and in this article we will analyze the recent confluence of events including 1) super contango due to OPEC+ conflict and 2) demand destruction due to the COVID-19 crisis, impact tanker vessel visits, and berth occupancy at the four major trading hubs.

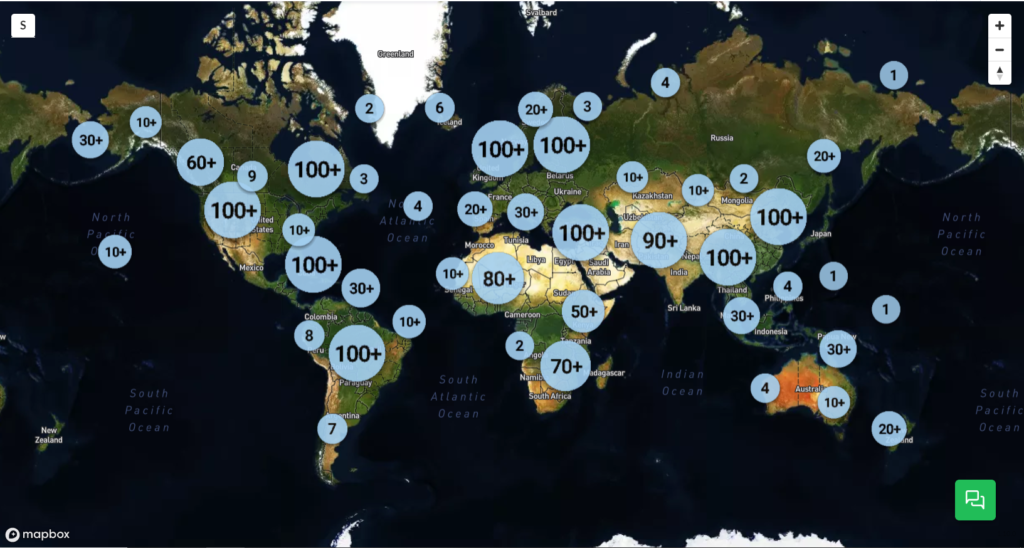

In the international oil and petrochemical market four main trading and storage hubs can be distinguished: ARA (Amsterdam-Rotterdam-Antwerp), Houston, Singapore and United Arab Emirates (UAE). Due to their large consuming backyard, their refinery infrastructure base and presence of a trading or financial industry, these hubs have become dominant regions in this trading industry.

Figure 1: Location of tank terminals around the globe; source TankTerminals.com

More details of the key trading hubs

The ARA consist of 68 terminals with a total capacity of around 36Mcbm. From these terminals, 65 terminals are marine terminals. Based on capacity the most dominant player is Vopak (9.2Mcbm) followed by Koole (3.5Mcbm), VTTI (3.2Mcbm) and Oiltanking (3.2Mcbm).

The port of Houston has 52 terminals with a capacity of approximately 29Mcbm. Main players are Kinder Morgan (6.3Mcbm), Enterprise Products (4.7Mcbm) and Magellan Midstream (4.2Mcbm). Of these terminals, 35 terminals have barge access and 24 terminals have sea access.

Singapore has 21 terminals with a total capacity of 16Mcbm. The biggest storage player in this area is Vopak (3.3Mcbm), followed by Oiltanking (2.5Mcbm) and Universal Group (2.3Mcbm).

The UEA consists of 61 terminals with a capacity of 18.5Mcbm. 20 of these terminals have sea access and 11 have barge access. The most dominant storage player is Vopak (2.6Mcbm), ADNOC (2.3Mcbm) and Horizon Terminals (1.7Mcbm). All these terminals are marine terminals.

“When deep-diving the global tank storage market and specific areas, it absolutely essential to understand how many storage capacity there is, how many players are active and what their position is”, according to Jacob van den Berge, Marketing and Sales Manager at IG. “This is the first step in defining the competitive landscape of the industry.”

Major events and their impact on storage demand further explained

Super contango due to OPEC+ conflict

What is contango? A contango is a situation where the price of front month oil futures is lower than oil with future delivery. If the spread between these prices is large enough to cover storage, finance and shipping costs, a trader is able to make a profit by buying oil now and selling it on the futures market for a later delivery. However, in order to capitalize on this profit, a trader needs storage (and transport) capacity. That is what happened in the first quarter of 2020 with massive demand for storage in ARA and the other key trading hubs resulting in high occupancy rates, putting a premium on free tank capacity now.

As the contango market structure persists and there is a lack of onshore storage facilities, traders are turning to tanker vessels to store their precious hydrocarbons.

This situation was heightened when Russia and Saudi Arabia could not come to terms regarding the height of production cuts to stabilize the fall in oil prices and Russia stepped out of the OPEC+ alliance. This resulted in Saudi Arabia offering its crude with huge discounts to its international customers, which triggered a free fall of oil prices and resulted in a super contango.

The recent peace between these two top producing countries and the subsequent OPEC+ deal has only reduced the speed of oil prices declining. The recent negative WTI oil prices show that we are far from balancing the market.

“Having an understanding of these key issues is imperative while calculating potential earnings,” says Chris Aversano, Product Manager at Q88.com. He continues, “Many of our products have earnings estimators that are built-in, giving our clients a greater understanding of the marketplace.”

Demand destructive impact of COVID-19

As we know, Coronavirus originated from China, and initially affected only China and its enormous economy. However, as the virus spread, different government lockdown interventions were initiated and economies came to a standstill. Less consumption, less production, less trade and less investments caused demand to be reduced significantly, all occurring in the first quarter of 2020.

A new feature in TankTerminals.com, called the Logistical Performance Benchmarking add-on, enables us to see what’s going on at terminals on a weekly basis. Amongst others, we can look at the activity levels at tank terminals.

So what did the numbers at the terminals of these major trading hubs show? Is there any impact of the super contango and COVID-19 crisis visible?

Putting It All Together

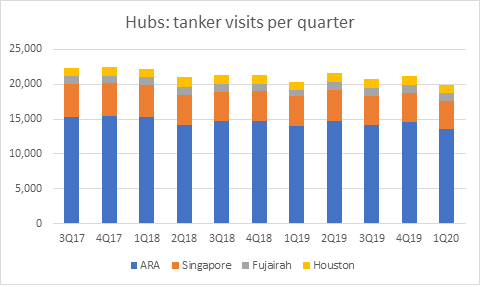

Tanker visits per hub per quarter

In figure 2 it can be seen that the number of tanker vessels visits at the marine terminals of the different hubs, ARA and Singapore show a similar pattern as applies for Fujairah and Houston. For ARA and Singapore applies that the peak of the visits were at the end of 2017 and the least visits in the first quarter of 2020. For Houston and Fujairah applies that highest number of tanker visits was in the second quarter of 2018 while the lowest number of tanker visits were seen in the first quarter of 2019.

Figure 2: Tanker visits per hub per quarter; source TankTerminals.com

The maximum value in ARA was 15405 tanker visits and the minimum value with 13591. In Singapore, the maximum value was 4756 and the minimum value was 3956. For Fujairah the maximum value was 1196 and the minimum value was 878. The maximum value in Houston was 1372 and the minimum value was 1153. As can be derived from the number of tanker visits, the ARA region accounts of almost 68% of all tanker visits of these four hubs combined. This is because of the extensive use of tanker barges and coasters in this area to distribute products within Europe.

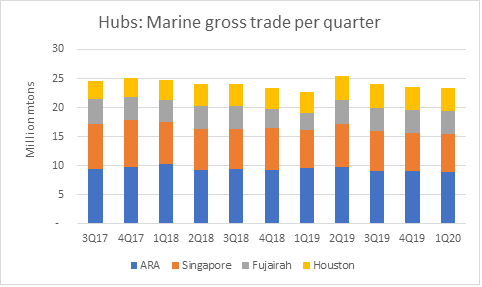

Marine gross trade per hub per quarter

Marine gross trade is calculated with the DWT of tanker vessels that loaded and discharged at a certain terminal. When we look closely at the marine gross trade trend and we compare that to the number of tanker visits, we are able to distinguish a similar trend as seen in figure 3 below.

Figure 3: Marine gross trade per hub per quarter; source TankTerminals.com

It is evident that the marine gross trade of the different hubs are more in line with each other. ARA accounts for 38%, Singapore 32%, Fujairah 18% and Houston 12% of the total sum of marine gross trade within these four regions. ARA is known for its intra- and inter- regional barge transports which contains lots of tanker visits with low volumes of product. Houston has a lot of push boat transports which are not included in this tool’s coding. Furthermore, we excluded Galveston and Beaumont area from the numbers.

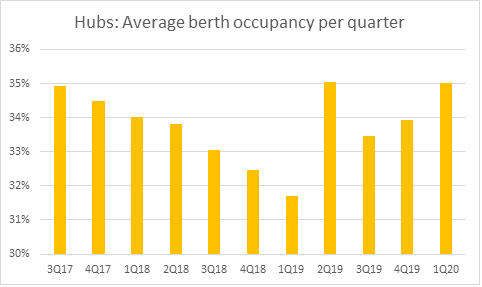

Berth occupancy per hub per quarter

Berth occupancy rates per region show a diverse picture on a quarterly base. However, some sensible deduction can be derived from looking at the data. For the regions ARA, Singapore and Houston, the average berth occupancy rates per terminal show a rather stable picture per quarter with minimum values around 31-32% and maximum values around 34-35%. Fujairah has a relatively inconstant structure with a minimum value at around 29% and maximum value just below 40%.

Figure 4: Average berth occupancy per quarter; source TankTerminals.com

It is evident from the chart above that the average berth occupancy rate for all hubs combined is the second highest in the first quarter of 2020. Across all regions, the data implies that average berth occupancy in this quarter is far above the average value. The decreasing trend up to the first quarter of 2019 highlights the ‘wait-and-see’ attitude leading up to the IMO 2020 marine fuel implementation. The peak in berth occupancy rates in the second quarter of 2019 and subsequent increases in berth occupancy since then can be explained as terminal operators were preparing for IMO’s legislation that went into effect at the beginning of 2020.

Conclusion and what is next?

When looking at the statistics of tanker visit numbers, marine gross trade and average berth occupancy rates, it can be concluded that the main trading hubs show similar patterns, especially in the second quarter of 2020 in which the defining events OPEC+ conflict and COVID-19 evolved.

In the first quarter of 2020 the number of tanker visits of the different hubs was at a minimum while the average berth occupancy rates were at their second highest. The low number of tanker visits is likely to have been caused by 1) high fill rate, or almost full tanks of terminal operators due to contango storage play options and 2) lower consumption levels due to demand destruction by COVID-19.

The high berth occupancy rates can be explained that, despite the low number of tanker visits, in the first quarter of 2020 terminal operators were coping with the impact of COVID-19 to their business operations which might have resulted in a bit slower vessel handling at the terminals.

“Knowing how well your ships are performing is crucial during these uncertain times,” say Chris Aversano, Product Manager at Q88. He continues, “Our VMS system gives the owners peace-of-mind to make the right decision at the right time. Additionally, our Position List platform allows for brokers to better serve their clients in a highly competitive and continuously changing space.”

Jacob van den Berge, Marketing and Sales Manager at IG adds: “using different data sets, combining this with our own unique knowledge and expert knowledge of our partners such as Q88 has proven to offer unique market intelligence. This supports our relations in making justified commercial decisions.”

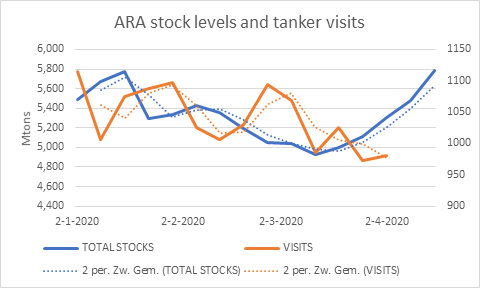

According to figure 5 below, when we focus in at the first quarter of 2020 and look at the tanker vessel visits in ARA on a weekly basis we see the number of tankers at terminal’s berths are all below this time series weekly average. If we than look at the ARA oil product stocks levels for the same time-period, we can actually see a buildup of stock levels since March 12. This in line when the lockdown measures that were initiated by the European governments.

Figure 5: ARA stock levels and tanker visits; source TankTerminals.com

Having access to accurate, up-to-date oil storage rates is crucial to make the right business decisions.

With our Global Oil Storage Rate Report, you’ll gain access to the single and only authoritative source of storage rate information available worldwide. It will provide you with transparency on price levels in global tank storage markets regularly, so you are always in the know and can set the right ask and bid prices for your storage.

Download your FREE Sample Report now and discover what information you could have at your fingertips each quarter.

DUBAI (Bloomberg) –The coronavirus that’s throttling fuel demand and forcing global producers to make unprecedented output cuts has left markets awash in so much crude that even the Middle East’s main oil-trading hub has run out of room to store unwanted barrels.

Terminal operators at Fujairah in the United Arab Emirates say they’re turning down requests from traders and refiners to store crude and refined products, whereas a year ago they had ample space. The port’s 14 million barrels of commercial crude-storage capacity is just a fraction of what Saudi Arabia and Abu Dhabi provide for their state oil companies.

Without tanks to lease, traders face costly constraints on their role as matchmakers who link a specific supply here with a willing buyer there. The global oil glut is making it harder for traders to even out imbalances in the market, and the plunge in crude, down about half this year, is making matters worse.

“If tanks are leased or blocked, then traders need to push back on taking crude,” said Edward Bell, senior director for market economics at Emirates NBD PJSC in Dubai. That, in turn, could force production in some places to halt, he said.

Demand for storage, an unglamorous but essential link in the global energy supply chain, is at its highest in years. From Singapore to Cushing, Oklahoma, tanks are brimming with crude, gasoline and other products, nowhere moreso than in Fujairah, a gateway for shipments from the world’s most prolific oil-producing region.

“The current capacity isn’t enough, for sure,” said Malek Azizeh, commercial director at Fujairah Oil Terminal FZC.

Even a deal between oil producers to trim global output by about a tenth won’t ease the storage crunch at Fujairah. The Organization of Petroleum Exporting Countries and partners such as Russia finally agreed on Sunday, after four days of deliberations, to cut production by 9.7 million barrels a day. Other nations, including the U.S. and Canada, expect to pump less because crude prices are too low for some of their oil companies to make a profit.

While a cut of this size would partly offset lost crude demand, it would fall short of OPEC’s own estimate for the drop in consumption. Trafigura Group sees oil use plunging by as much as 35 million barrels daily — roughly a third of normal global output — as countries prolong lockdowns over the coronavirus.

Fujairah, which hugs a ribbon of coastline between the craggy Hajjar Mountains and the Gulf of Oman, cemented its position in the world’s oil-storage and supply network over the last 30 years. It started out as a refueling station for tankers shunting crude from the Persian Gulf to refineries in China, the U.S. and elsewhere. It also built tanks where traders could stockpile fuels.

As state producers Saudi Aramco and Abu Dhabi National Oil Co. boosted refining capacity and started their own trading units, Fujairah’s storage operators benefited from the increasing volumes of crude and refined products flowing to and from the Gulf. Now that refineries are processing less crude and many of the world’s vehicles and aircraft are at a standstill, those regional flows have dwindled.

Stockpiles of fuel oil and other heavy distillates at Fujairah swelled more than 30% in the past year to 15.4 million barrels, according to the Fujairah Oil Industry Zone, which oversees the city’s terminals. Local authorities don’t provide inventory data for crude oil.

Two projects to add more than 62 million barrels of storage won’t be built until next year at the earliest.

“We are going to run out of storage because the demand declines are so steep,” Amrita Sen, chief oil analyst at Energy Aspects, said in a Bloomberg Television interview.

By ANTHONY DI PAOLA AND VERITY RATCLIFFE on April 13, 2020

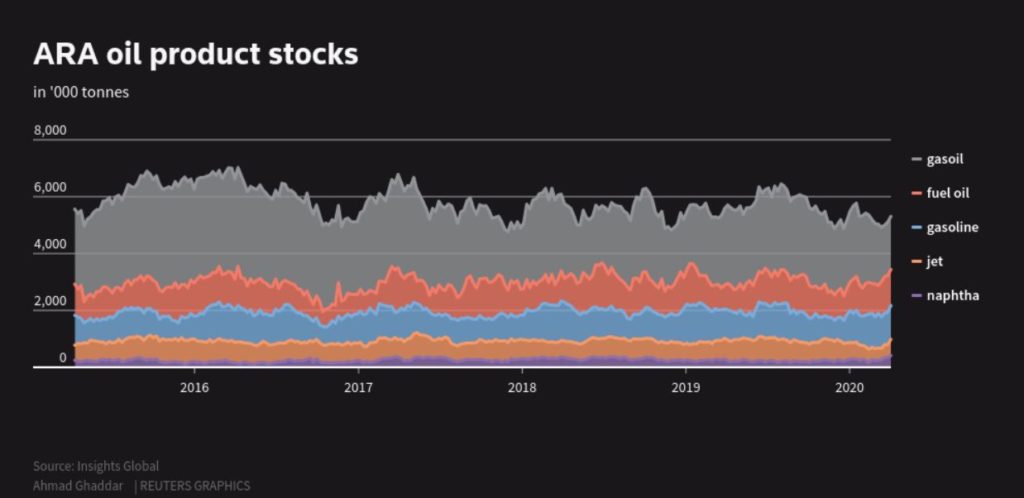

LONDON, April 8

(Reuters) – Independently-held storage tanks for oil products in the

Amsterdam-Rotterdam-Antwerp hub may be already fully committed to traders, but

utilisation levels are still at around the halfway mark, Dutch consultants

Insights Global said.

With demand for fuels across Europe in free fall from the

lockdowns that the new coronavirus outbreak has caused around the continent,

and the subsequent price crash for many fuels, traders have been on an oil

storage binge.

But while they been booking a place in those tanks, the

tanks are as of the latest data only at around 50-60% full.

“There is hardly any, or more likely no tank

capacity available in ARA for lease right now. Everything is booked out,”

managing director for Insights Global Patrick Kulsen said.

Gasoil and diesel tank utilisation, for example, stood at

48.73% on April 1, compared with nearly 80% at the start of the year.

One explanation for the low utilisation level has been

increased demand from inland markets in Germany and Switzerland for

stockpiling, Kulsen said.

But as demand for fuels continues to be battered by

millions of people staying at home, tanks are expected to fill to the brim,

analysts expect.

Consultants Rystad Energy forecast oil demand in Europe

in 2020 falling by 2.3 million barrels per day to 12.7 million bpd, an 11.2%

decline from 2019’s 14.3 million bpd. They expect Europe’s April road fuel

demand to fall by 35% to 4.7 million bpd.

Reporting by Ahmad Ghaddar; editing by David Evans

GDPR Consent

Our website uses cookies. Click on the 'Accept all' button to accept the cookies and on the 'Settings' button for more information and settings.