The impact of ARA barge transport on the feedstock within the petrochemical sector.

| Naphtha is an intermediate hydrocarbon liquid stream derived from the refining of crude oil. It is in the ARA region mostly used as a gasoline blending component as feedstock within the petrochemical sector. Other important feedstocks for the petrochemical sector include ethane, propane and methane. The petrochemical sector is responsible for producing various materials such as plastic, paints, solvents, fibres and raw materials for pharmaceutical and cosmetics sectors. |

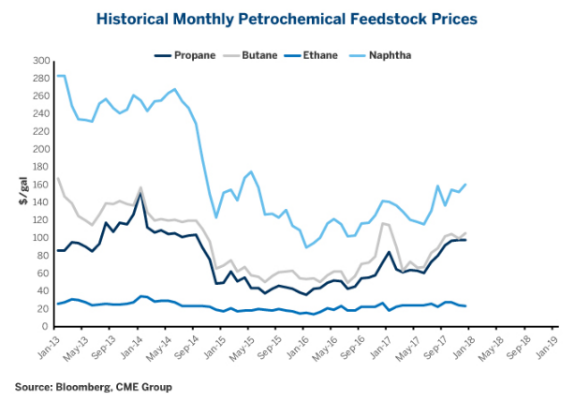

| The ARA-region, or Amsterdam – Rotterdam – Antwerp region is an area in The Netherlands and Belgium where various coastal and inland ports are interconnected and act as a global hub. Apart from the large ports Amsterdam, Rotterdam and Antwerp it includes Flushing, Ghent, Terneuzen and Moerdijk as other relevant ports. All these ports lie in the delta of various rivers, like the Rhine, Meuse and Scheldt, which flow into the North Sea and could be seen as gateway of the European continent. Hinterland markets are connected to global markets via these seaports, in particular the vast hinterland of German industrial centres and population. The river Rhine, Scheldt and Meuse enable barge transport to and from these ports to inland markets, which give the market its unique attractiveness and improves the position of the hub in the worldwide trade flows. When we take a closer look at the feedstock prices we can observe that naphtha is the most expensive feedstock. In the image below you can see the historical monthly petrochemical feedstock prices from 2013 till 2018. |

Although naphtha is the most expensive feedstock, it is the most used feedstock in the ARA region of all the substitutes mentioned above. There are various factors influencing this, but in this article we focus solely on the barge transport. As we have established earlier the Rhine has a unique position as being an important route for the transport of liquid bulk across different Western European countries. It is one of the world’s most frequented inland waterways. In Europe, there are more than 13.500 vessels offering inland freight transport services (dry cargo, tanker cargo and push & tug vessels) with a total loading capacity of 17 Mio tonnes. About 76% of the European fleet comes from Rhine countries. Source : Inland Navigation Europe. Tankers account for +- 15% of the total inland fleet.

Of the liquid bulk market, according to PJK’s interntional numbers you can see in the image below a comparison of the number of inland tankers showing that the clean (including chemical) tankers are far more dominant compared to gas tankers. While there are currently more gas tankers under construction, the same accounts for clean tankers. Clean tankers under construction are also bigger in terms of DWT, up to 10,000 DWT.

| As mentioned before, naphtha is a liquid hydrocarbon mixture, which means it should be transported in double hull tanker, mainly to prevent cargo from leaking due to its hazardous nature. With regard to ethane and propane it is different as these are gases, and therefore have to be transported in special gas tankers, which are often fabricated with triple hulls and equipped with circular tanks. At the moment there are far more double hull tankers available in the market compared to the gas tankers, increasing supply of transport possibilities. Therefor the transport of naphtha is economically more feasible and accessible, despite the higher product costs. Another reason for the high usage of naphtha in the region is the excess components received after cracking naphtha. These residues are used in the gasoline blending market, which holds a key position in the ARA and provide more usages of the excess valuable components like for example isomerate, raffinate, toluene and xylene. As you can see a lot of factors influence the petrochemical market. Are you struggling to connect the dots of the petrochemical side of the cluster? We can then provide you with our ARA Petrochemical Tank Storage report, where we aim to shed some light on complex subjects by unravelling trends and themes that underlie current markets relevant for the ARA cluster and by giving an outlook for future states of these petrochemical markets. |

| Contact us at our headquarters in the Netherlands at +31 (0) 850 66 25 22 |

| The contents of this article from Insights Global has been written with the greatest possible care. However, Insights Global cannot guarantee the accuracy or completeness of the information. The content of Insights Global blog publications therefore are not legally binding. Insights Global accepts no liability which might arise from the content of its blog. |